I have this tendency to publish a post each January about what I see coming in the New Year. I’m a little late this year (being it’s already January 20th), but that’s because the general mood has been leaning negative of late — not exactly motivating for an optimist like me.

I refused to use an AI-generated image this time. I instead chose this awesome photo by Nicole Avagliano via Unsplash.

Then again, my post in January 2023 wasn’t real upbeat, either. But that was more of a tongue-in-cheek exercise. The previous year, my post in January 2022 wasn’t a list of predictions, but rather focused on one big positive trend I couldn’t ignore: the startup boom. (Remember those good old days?) Going back to January 2021, I went full-on optimist, though had some fun with it, as we were coming out of that God-awful pandemic year and needed some levity.

Anyway, for this post, I finally got around to fleshing out the notes I’d been making over the past couple of weeks. I tend to not blurt things out — I like to think a bit first. (Call me crazy compared to most bloggers… haha.) This year, I went beyond tech to some other topics I just find hard to ignore these days. So here goes:

• AI … The hype curve has peaked. Enjoy the ride down into the trough of disillusionment. I won’t say anything more because… are there any more words to say at all that haven’t already been said about AI in 2023? A breather is needed for sure, because the hype has been getting out of control as we sit here in early 2024. (Note: I am not anti AI, I am anti *AI hype* and anti *AI washing*, which so many startups are doing in an attempt to raise money.) A funny recent quote I saw is from Philip Elmer-Dewitt, who runs the very popular Apple 3.0 news blog: “I’ve been following the A.I. beat since Ronald Reagan’s first term, and in my experience its champions have consistently over-promised and under-delivered. Large language models and generative A.I. are real things, but so are self-driving cars and they’re still running over pedestrians.”

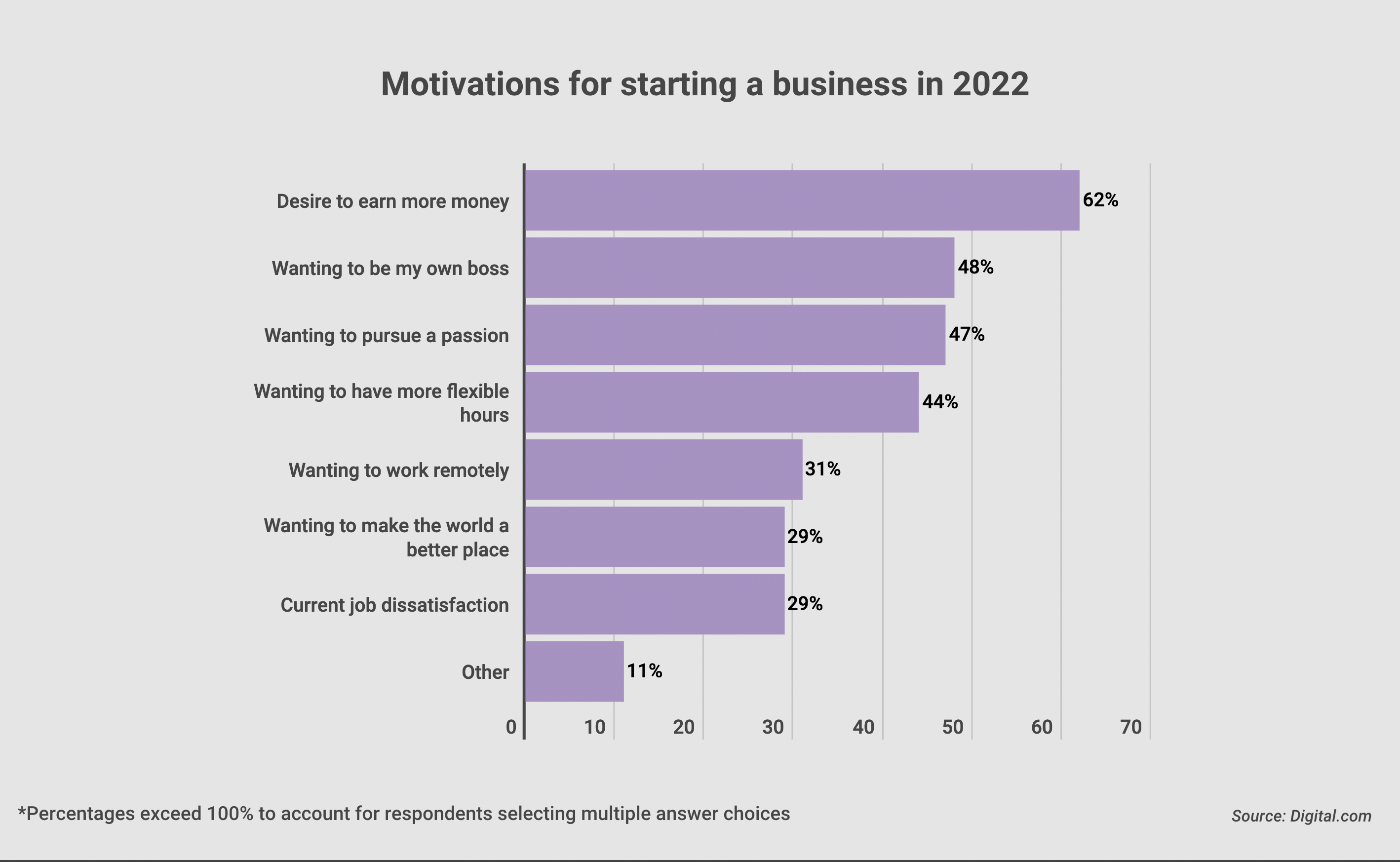

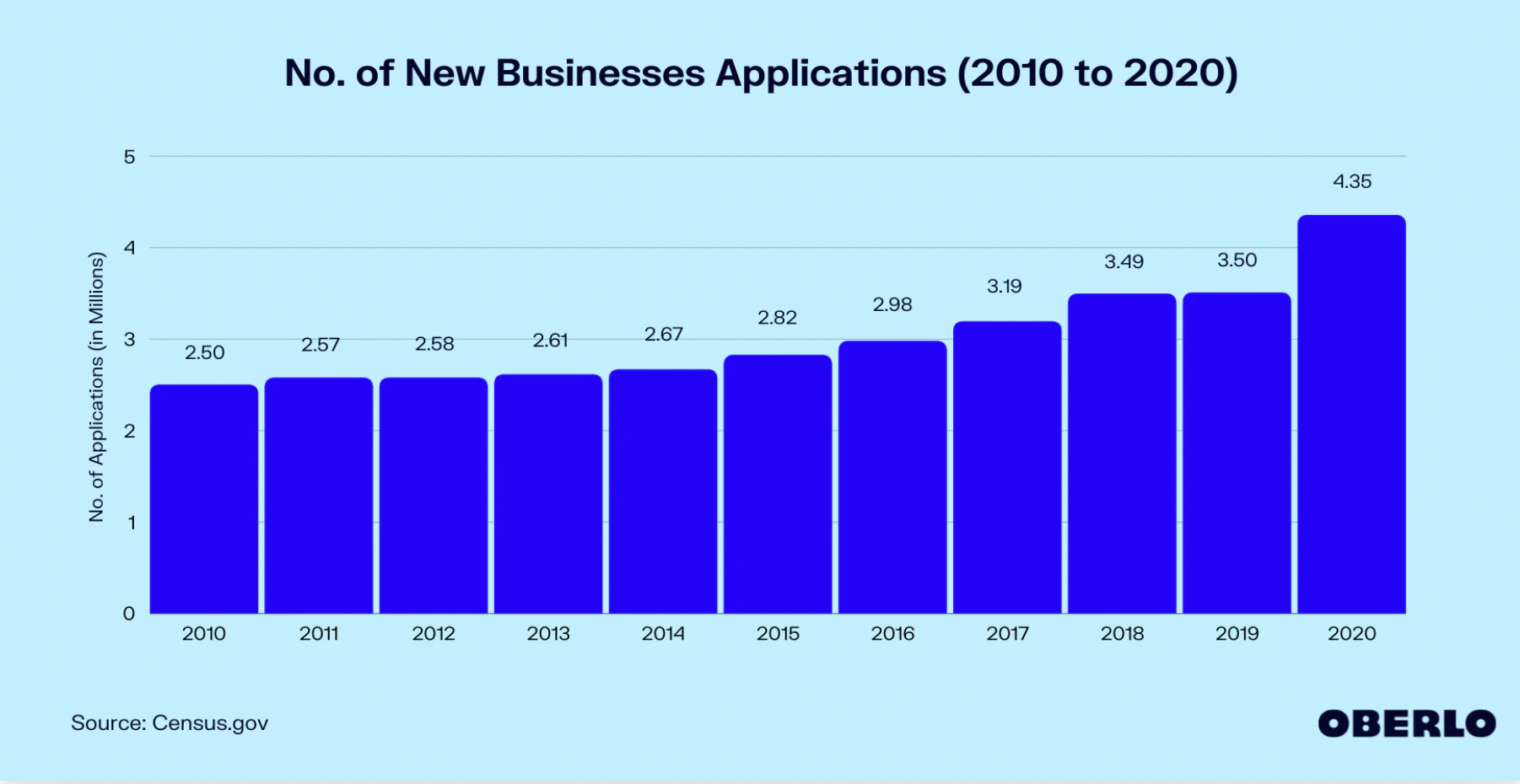

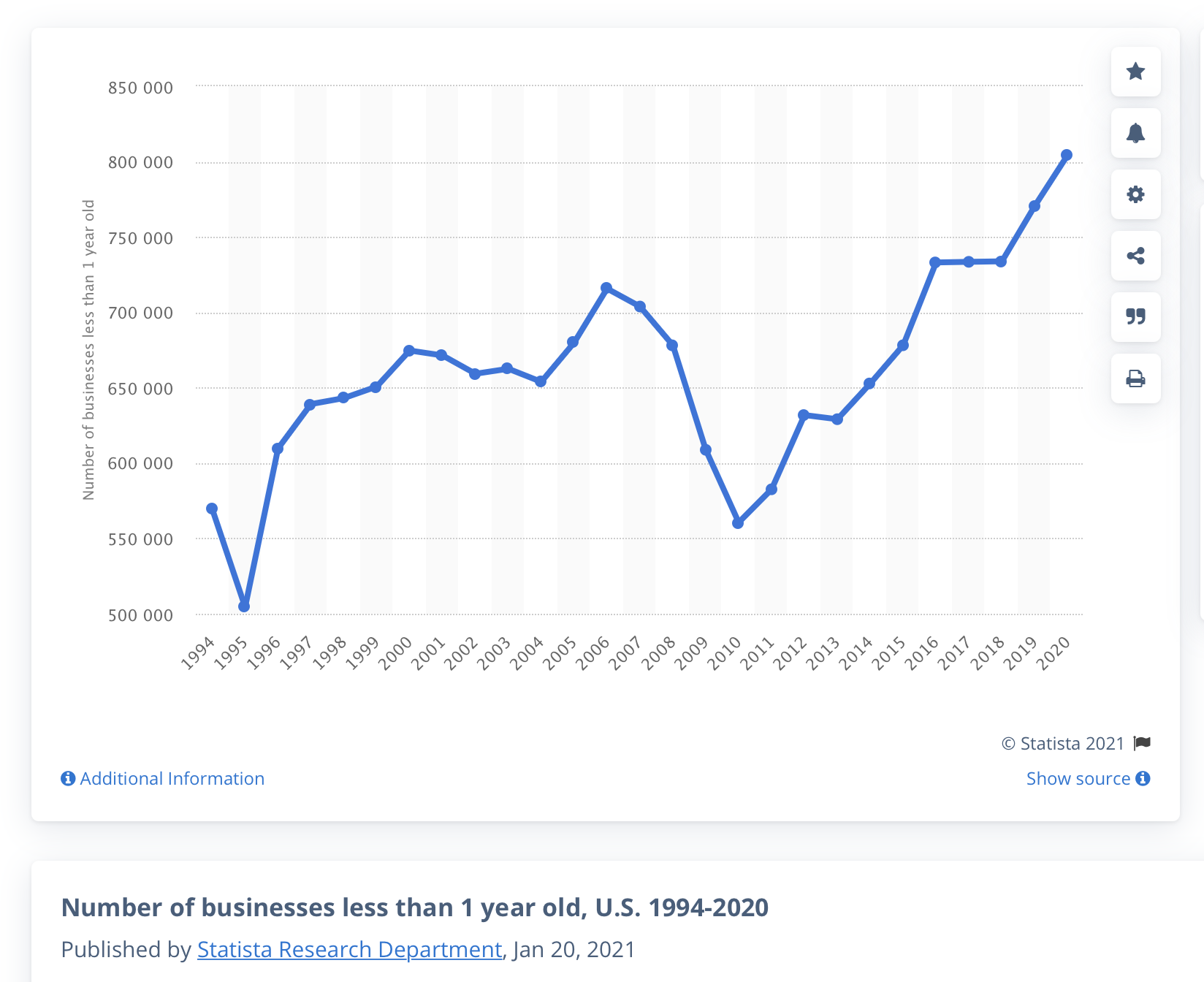

• Startups … According to AngelList, the startup formation number was well down in 2023 — 40 percent since 2021! That’s horrible. I predict the number will pick up somewhat in 2024. However, a meaningful reversal won’t come until 2025 with a new administration.

• VC … In 2024, I will not be surprised if more VC funds shut down. (A big one did last month.) And check-writing from those that have been largely sitting on their hands in 2023 may not increase much. The numbers are sobering. Pitchbook reported in December that 38% of VCs “disappeared from dealmaking in 2023.” Pitchbook also reported that VC investors injected only $170 billion into startups in 2023, a decrease of nearly 30% from the $242 billion recorded in 2022. In 2021, the number was $348 billion. Not a pleasant trend.

• Apple … My price target for $AAPL shares is $220 by yearend — on the strength of the iPhone 16 in the fall (call it “the AI phone”), advancements with the next Watch, and, yes, the initial success of “spatial computing.” No Apple Car anytime soon, friends. Which is fine with me.

• Sports / National … Will gambling on NFL games get out of control? One senses that a crackdown must be coming. Right on cue, Minnesota legislators are trying to have sports betting legalized in our state. I for one am getting really sick of all the gambling hype!! On another topic, with TV commercial time absolutely ballooning to fund NFL largesse, I predict sales of low-cost DVRs, like the $79 Tablo unit (to record live TV and certain streaming channels), will boom — letting consumers without high-cost cable services (like that rascally DirecTV) inexpensively record and watch just the actual game, skipping through the mind-numbing amount of commercials they now blast at us. And no subscription is required.

• Sports / Local … The Vikings will do better. Which isn’t saying much. And Gopher football damn-well better improve as well! 2023 was embarrassing. One highlight in 2024: we’re finally going to the Rose Bowl! Okay, it’s only a regular season matchup October 12th against UCLA (in their home stadium), as they become part of the Big Ten (Big 18!) this year. And another glaring college football topic: I fear, as many do, that NIL is ruining the sport (sigh). It’s the main reason Nick Saban resigned as coach at Alabama, Hey, we don’t need more “professional” sports!

• Higher Ed … College enrollments will continue to drop nearly everywhere, but prices will of course not fall nearly as fast… if at all? That tells you all you need to know. How bad is higher education? Americans’ confidence in these institutions has dropped from 57% in 2015 to 36% in 2023, according to a July 2023 poll by Gallup. Here’s more, from Barron’s: “College tuition rose 12% on average annually from 2010 to 2022, according to data compiled by the National Center for Education Statistics and the U.S. Bureau of Labor Statistics. After adjusting for inflation, college tuition has increased 747% since 1963.” This prediction I don’t make joyously, as two startups in my portfolio are in this space. (Luckily a small percentage.)

• Minnesota State Government … Complete DFL control will end — it has to! Hope you enjoyed watching that $18 billion surplus — your money — go poof! That measly $520 rebate check to taxpayers (per couple) was an insult. But you fellow Minnesotans already knew that. More people are leaving the state than the number moving in. It’s not just the weather.

• Minneapolis … The city will never be the same, I am convinced. And St. Paul, which is suffering almost as badly (worse with tax increases), shares the same fate. The population of both cities will continue to drop.

• Anywhere But the City … Within the state, the escape from the central Twin Cities to the metro area suburbs and rural MN will continue, as will the rise in values for lakefront property, hobby farms, and farmland. I included some great insights into the trend toward remote work outside the cities, from a national viewpoint, in a post I published in January 2021.

And one more prediction for good measure:

• The Media Business …. Let me go out on a limb 🙂 — the media industry will continue to contract in 2024. Many more jobs will be lost. Take a guess how many — then double it. One glaring reason: according to an October 2023 Gallup poll, a record-high number of Americans — 39% — say they don’t trust the media at all. That number has steadily increased since 2018.

So, on we go. (Yes, to a brighter 2025.)

———————————————

Postscript:

And in my continuing quest to counter the AI hype, I give you this:

A Technologist Spent Years Building an AI Chatbot Tutor. He Decided It Can’t Be Done.

———————————————

And Another Postscript:

I saw a Wall Street Journal Saturday Essay recently (subscription required) entitled “Why Americans Have Lost Faith in the Value of College.” In it, they noted that the decline in undergraduate enrollment since 2011 has translated into 3 million fewer students on campus. Nearly half of parents say they would prefer not to send their children to a four-year college after high school.

Billionaires who slam higher ed also don’t do it any favors. Here’s Elon Musk on the topic in 2020:

“College is basically for fun and to prove that you can do your chores, but not for learning. I don’t consider going to college evidence of exceptional ability. In fact, ideally, you drop out. You don’t need college to learn stuff. Did Shakespeare go to college? Probably not.”

As a former English major, I can attest… 🙂

———————————————-

And Yet ANOTHER Postscript:

Re: my VC prediction, here’s additional insight into the state of the industry:

Okay, that’s enough postscripts for one post. I publish insights like these to my X account as well, so please follow me there, where I post daily. Over and out!

Recent Comments